For decades, financial institutions and their practices have often favored remaining antiquated rather than following innovation and opening themselves up to outside influence. As the age of technology dawned on us, many financial institutions and companies were able to bear the fruits of this new adoption. Now, it has become a necessity to succeed, and one cannot separate themselves from the competition with it.

With the improvements in the technology field, financial institutions have been forced out of comfort and into the open lens that the world has become accustomed to now. With all sorts of different companies, such as clothing manufacturers and fast-food companies having to be more transparent about their front and back-end operations, it was normal for finance to follow as well. With that comes open finance. Essentially, this means users can share and use their financial data through third parties. This is done through application programming interfaces (APIs). In layman’s terms, this is a way to give authorized third parties one’s required financial data in a safe and secure manner.

At first, this might sound slightly frightening, but it is likely that most of us are actively participating in this already. For example, when we use payment services such as GooglePay or Paypal, we authorize these third parties to access our banks as long as we enter our passcode. Similarly, Apple Pay can utilize its highly secure FaceID feature (in the phones that have it) to facilitate an even more safe transfer of funds. Furthermore, it uses a near-field communication chip in the back of its newer devices to make in-person payments by simply holding the phone close to a card swipe machine (payment terminal) to authorize a payment. It can also be used in other financial relationships such as mortgages, pensions, loans, and asset management.

Read More: The Rise of Sustainable Finance: 2022 Impact Investment Trends

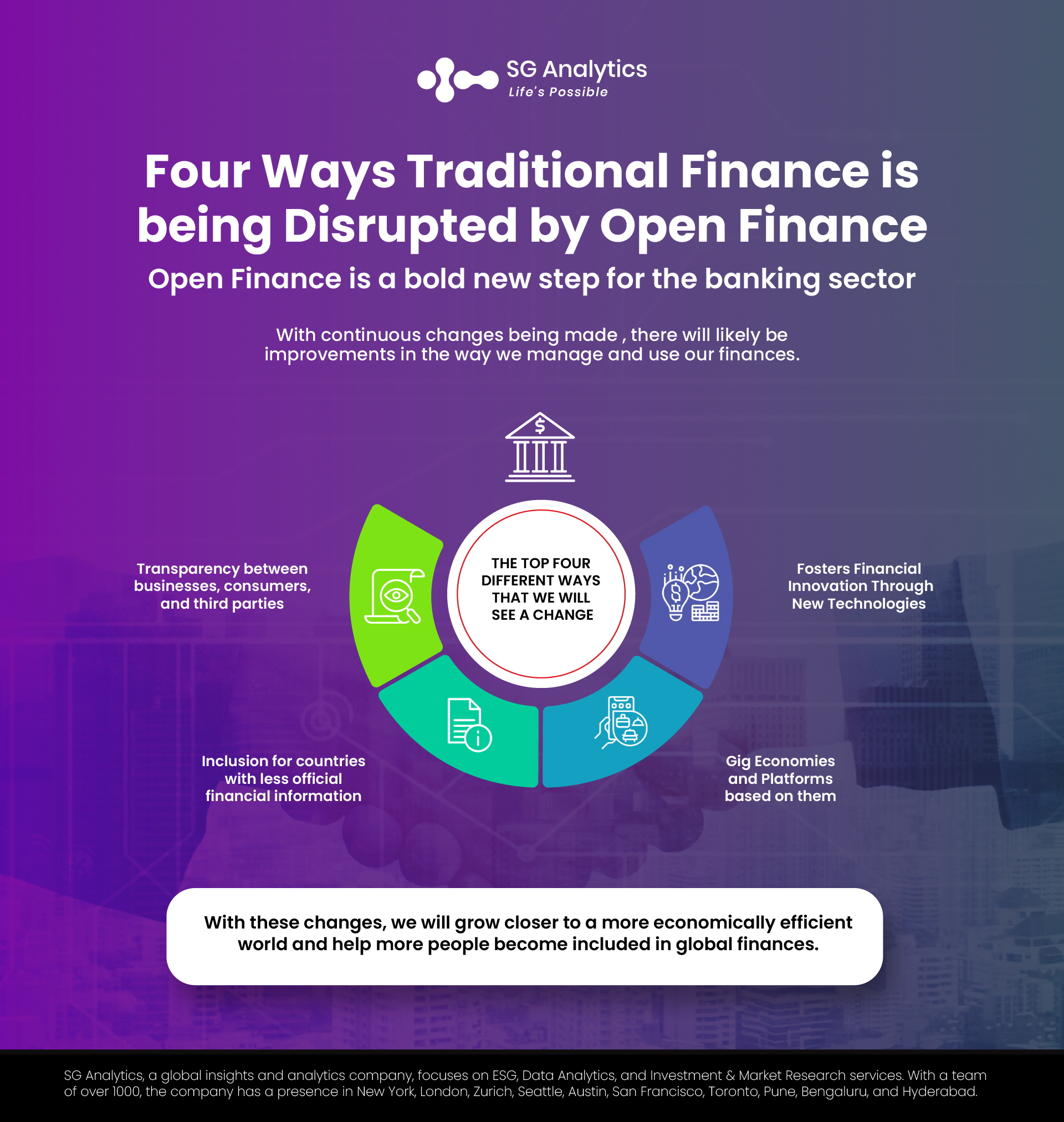

Why Finance companies should embrace Open Finance:

-

Transparency between businesses, consumers, and third parties

-

Inclusion for countries with less official financial information

-

Gig Economies and Platforms based on them

-

Fosters Financial Innovation Through New Technologies

-

Transparency between Businesses, Consumers, and Third Parties

In the past, many services built on users’ financial data had to resort to data scraping. This is a technique that uses a script to find all public data on user finances. However, it is quite inefficient, and because of the lack of active participation, businesses aiming at developing new financial services are unable to gain key insights through market research as to whether this will be possible. In the new situation, data transparency has proved to be extremely beneficial for all parties involved.

For service providers and banks, conscious transparency means that the banks can ensure the secure sharing of data and avoid friction in programming solutions. Furthermore, the banks can control how much data is shared so that the process remains seamless, but unnecessary personal data is not transferred.

As for consumers, we are likely already reaping the benefits of open finance. However, there are many more applications that we can use to make our navigation of the financial world more ideal. For example, many developers are releasing applications that connect to your bank accounts to keep track of finances. This helps to categorize your monthly finances and support your budgeting needs. Other developers have also come up with apps that are able to link your many different bank accounts in one place so you can gain a holistic view of your current financial situation as well as the bills that needs to be paid. Furthermore, all payments are placed in the same place, and services like Google Pay can help you pay phone, electricity, and other bills along with general purchase payments as well.

Read More: Data & Analytics Strategy: Must-Have Crucial Elements for Decision Making

-

Inclusion for Countries with less official Financial Information

In many lesser developed economies, a lot of the financial transactions do not take place through banks. While this means it is not documented, for the most part, it is hard to gauge the flow of money within the economy without the use of open finance tools. In the case of governments, it is more challenging to create effective economic policies due to the lack of understanding of the economic situation. This means that legislative decisions would have to be made based on limited understanding. Similarly, companies and developers looking to launch new solutions will also struggle as they cannot garner a strong database to understand the demographic that they will be launching to. As a result, many MNCs choose not to release certain applications in these countries as it becomes more difficult to make large investments without a large knowledge base.

A good example of the benefits of open finance, in this case, is Minu, a Mexican application. It is a pay-on-demand service for employers to pay their employees. It creates a seamless method of transferring paychecks while bypassing the banks. Users can gain access to their funds immediately and are able to see their balance right away without having to worry about any additional fees other than the set fee that is required at withdrawal. Furthermore, employees can gain access to a paycheck early as many of the users work daily change, which means that (while the payroll is already scheduled) they can gain access to this money early in urgent cases. This is extremely important for financial inclusion, and apps like this work extremely well in improving economic efficiency and resource allocation.

-

Gig Economies and Platforms based on them

As mentioned earlier, many employees work on a day-to-day basis. Essentially, they do not have a set paycheck and earn different amounts on different days. Whether this means they are Uber drivers, and their pay is variable based on the frequency and length of their journeys, or they are IT technicians, and their compensation depends on the difficulty and duration of the jobs, many nations have seen burgeoning gig economies.

This was generally quite difficult to manage as most of these freelancers would have to go door to door or rely on word of mouth to ensure that their services reached the customers. For many, marketing costs were too high to bear, and they struggled because they were unable to educate the consumer on their services. However, with open finance, many of these problems have been solved. A large example of this has been delivery drivers. With large companies like UberEats and Doordash as well as smaller domestic food delivery companies, restaurants can gain a much large reach. Moreover, delivery drivers can find work by simply being on the app and accepting orders meaning that the amount they make is much less variable.

-

Fosters Financial Innovation through New Technologies

Although many of the previously mentioned applications might be favored by the banks because of their efficiency, there are certain applications that the banks might be against. This is because many of these solutions involve “cutting out the intermediary,” which normally means the banks. For example, banks make massive amounts of money on international transactions every day. This means that they can charge large fees as well as use exchange rates that favor them when authorizing transactions. For many years, this remained lucrative as it was the only option available. Short of exchanging currency in one country and simply carrying the cash over, one had very limited options in terms of making large transfers. However, with the help of open finance, companies like Wise (formerly known as TransferWise) help people make large transfers to different currencies for a fraction of the cost. To stay operational, they still take a fee based on the transaction size. However, it is quite meager and ensures that you lose very little when making the exchange.

Furthermore, Cryptocurrencies and blockchain-related solutions have made it so that people can get loans at extremely low-interest rates. In many countries, banks run the monopoly on deciding how much interest one must pay on loans, so newer solutions might also force banks to come closer to the national mandates and not take as much of a cut.

Read More: NFT Digital Art: The Technology that is Transforming Creativity

A Bold Step Forward

As it has become clear over the years, transparency is the best policy going ahead. The main intention of most of this was to improve economic efficiency and open the channels to ensure collaboration between different sectors and finance. Finance has remained an elusive and slightly disconnected sector from the others. However, the new age of open finance is sure to disrupt the field with innovation coming in, in all different fields.

Furthermore, this has also massively benefited the lower and middle class in developing economies as it has enabled better employment opportunities while also facilitating a more financially inclusive environment for all. This not only helps individual citizens but is likely to be imperative in the overall development of the economy.

With a presence in New York, San Francisco, Austin, Seattle, Toronto, London, Zurich, Pune, Bengaluru, and Hyderabad, SG Analytics, a pioneer in Research and Analytics, offers tailor-made services to enterprises worldwide.

A market leader in Investment Research Services, SG Analytics assists in strengthening investment decisions by leveraging custom research support. Contact us today if you are in search of an investment research firm that offers tailored research support across a broad range of asset classes.